Yes, the short answer is that your health insurance almost certainly covers rehab. Thanks to federal laws like the Affordable Care Act (ACA), insurance companies are required to treat substance use disorders just like any other medical issue, such as diabetes or heart disease.

This legal protection means your policy should provide benefits for crucial recovery services, including detox, therapy, and ongoing care. However, knowing you have coverage is one thing; understanding how it works is the key to using it effectively.

Key Takeaways

- Coverage is a Legal Right: Federal laws like the Affordable Care Act (ACA) and the Mental Health Parity and Addiction Equity Act (MHPAEA) mandate that insurance plans cover addiction treatment similarly to other medical conditions.

- Understand Your Plan's Details: Your plan type (HMO, PPO) and financial terms (deductible, copay, coinsurance, out-of-pocket maximum) directly determine your costs and which facilities you can use.

- Verification is Non-Negotiable: Always call your insurer to verify benefits and secure pre-authorization before starting treatment to avoid denied claims and unexpected bills. The rehab center's admissions team can help with this process.

- In-Network is More Affordable: Choosing an in-network rehab facility will almost always result in significantly lower out-of-pocket costs compared to an out-of-network provider.

Decoding Your Insurance Plan for Rehab Treatment

Let's be honest: trying to make sense of an insurance policy can feel overwhelming. It's filled with jargon, acronyms, and fine print that can feel like a maze, especially when you're already dealing with the stress of seeking help. This guide will help you cut through the noise and understand your insurance coverage for rehab in plain English.

Your right to treatment is built on the foundation of two crucial laws: The Mental Health Parity and Addiction Equity Act (MHPAEA) and the ACA. Together, they ensure that addiction treatment isn't treated as a second-class medical need.

These laws established what's known as "parity." In simple terms, it means insurers can't place stricter limits on your addiction treatment benefits than they do for medical or surgical care. Your coverage for rehab should be just as robust as your coverage for a broken arm.

While this gives you a strong starting point, the specific details of your plan will ultimately shape your path forward.

What Kind of Insurance Plan Do You Have?

The type of health insurance plan you have—whether it’s an HMO, PPO, EPO, or POS—is like the rulebook for your treatment journey. It determines which rehab centers you can go to, whether you need referrals, and how much flexibility you have. Figuring this out first will save you from headaches and unexpected bills later.

Here’s a quick rundown of what those acronyms really mean:

- HMO (Health Maintenance Organization): With an HMO, you generally have to stick to doctors and facilities within their pre-approved network. You’ll also likely need a referral from your primary care physician before you can get addiction treatment covered.

- PPO (Preferred Provider Organization): PPOs give you much more freedom. You can see providers both inside and outside the network without a referral, but you'll pay a lot less if you stay in-network.

- EPO (Exclusive Provider Organization): Think of this as a hybrid. You don't need a referral to see a specialist, but you must use providers within the plan's network (except for true emergencies).

- POS (Point of Service): This plan mixes HMO and PPO features. You might need a referral like an HMO, but you often have the option to go out-of-network for a higher price, similar to a PPO.

Knowing your plan type is the first step to narrowing down the list of rehab centers that are realistic options for you financially.

Getting a Handle on the Financial Terms

Beyond your plan type, a few key financial terms directly control how much you'll actually pay out of pocket. Getting familiar with this vocabulary is the best way to predict the real cost of treatment and avoid any nasty surprises.

To start, let's simplify the most common terms you'll encounter when discussing insurance for rehab.

Key Insurance Terms for Rehab at a Glance

| Term | How It Affects Your Rehab Costs |

|---|---|

| Deductible | This is the fixed amount you must pay for treatment before your insurance starts to pay anything. You have to meet this first. |

| Copayment (Copay) | A set fee you pay for a specific service, like a doctor's visit or therapy session, after you’ve met your deductible. |

| Coinsurance | This is a percentage of the total cost that you share with your insurer. For example, they might pay 80% while you pay the remaining 20%. |

| Out-of-Pocket Maximum | The absolute most you will have to pay for covered services in a plan year. Once you hit this limit, your insurance pays 100%. |

Think of your deductible as the initial hurdle you have to clear. Once you've paid that amount, you'll only be responsible for your copays and coinsurance until you hit your out-of-pocket maximum. Understanding this flow of costs is essential for planning your recovery without financial stress.

What Rehab Services Your Insurance Actually Covers

It’s a huge relief to know your plan includes insurance coverage for rehab. But the next logical question is, what does that actually mean? What services get a green light? Your policy isn't just a simple yes or no; it's a key that unlocks different levels of care designed to meet you where you are on your recovery journey.

Think of addiction treatment less like a single event and more like a path with several distinct stages. Each stage requires a specific kind of support, and insurance companies structure their benefits to cover this entire continuum of care. This ensures that as your needs evolve, your coverage can adapt right along with you.

The First Step: Medical Detoxification

For most people, the journey begins with detox. This is the critical first step where your body safely clears itself of substances under the watchful eye of medical professionals. Withdrawal symptoms can range from deeply uncomfortable to genuinely dangerous, which makes this supervised care absolutely essential.

Because of this, detox is almost always considered a medical necessity and is a covered service. Insurers understand that a safe, medically managed withdrawal is the only responsible way to build a foundation for lasting recovery.

Inpatient and Residential Treatment Programs

Once detox is complete, many people transition to an inpatient or residential program. This is an immersive level of care where you live at the treatment facility 24/7. It’s a structured, supportive environment designed to remove you from the triggers and stressors of your daily life so you can focus entirely on healing.

This intensive setting is perfect for those with severe substance use disorders or for individuals also dealing with co-occurring mental health conditions. As long as it's deemed medically necessary, your insurance plan will typically cover the major costs of your stay, including room and board, meals, and a full schedule of therapeutic services.

A study found that individuals who completed residential treatment were significantly more likely to remain abstinent one year later compared to those who did not. This data supports the medical necessity that insurers look for when approving inpatient stays.

Flexible Outpatient Treatment Options

Living at a facility isn't the right fit for everyone. That’s why insurance also covers different levels of outpatient care. These programs provide powerful, effective treatment while giving you the flexibility to live at home and continue managing work, school, or family commitments.

The two most common forms of intensive outpatient care are:

- Partial Hospitalization Programs (PHP): Think of PHP as a step down from residential care but a step up from traditional therapy. It's the most intensive outpatient option, often requiring you to be at the facility for several hours a day, five to seven days a week.

- Intensive Outpatient Programs (IOP): An IOP is a bit more flexible than a PHP. It still provides a strong, structured support system but typically involves fewer hours—just a few hours a day, a few times a week.

Both PHP and IOP are standard covered benefits because they offer a cost-effective way to deliver high-quality, structured care without the expense of 24/7 residential services.

Core Therapeutic Services Your Plan Covers

Whether you’re in an inpatient or outpatient setting, your insurance coverage will pay for the core therapeutic services that are the real engine of recovery. These are the fundamental building blocks of any quality treatment program.

You can expect your benefits to include:

- Individual Therapy: Private, one-on-one sessions with a licensed therapist to dig into the personal issues and root causes driving the addiction.

- Group Therapy: Professionally guided sessions with your peers. It’s a space to build community, share struggles and successes, and realize you aren't alone.

- Family Counseling: Therapy that brings loved ones into the process to help heal damaged relationships and build a strong support system back home.

- Medication-Assisted Treatment (MAT): This combines FDA-approved medications (like buprenorphine or naltrexone) with counseling to treat opioid or alcohol use disorders, helping to manage cravings and withdrawal symptoms.

These services are the cornerstones of modern recovery. To see why they are so effective, you can learn more in our guide to evidence-based addiction treatment. Insurance companies cover them because their success is backed by years of research, making them a smart investment in your long-term health.

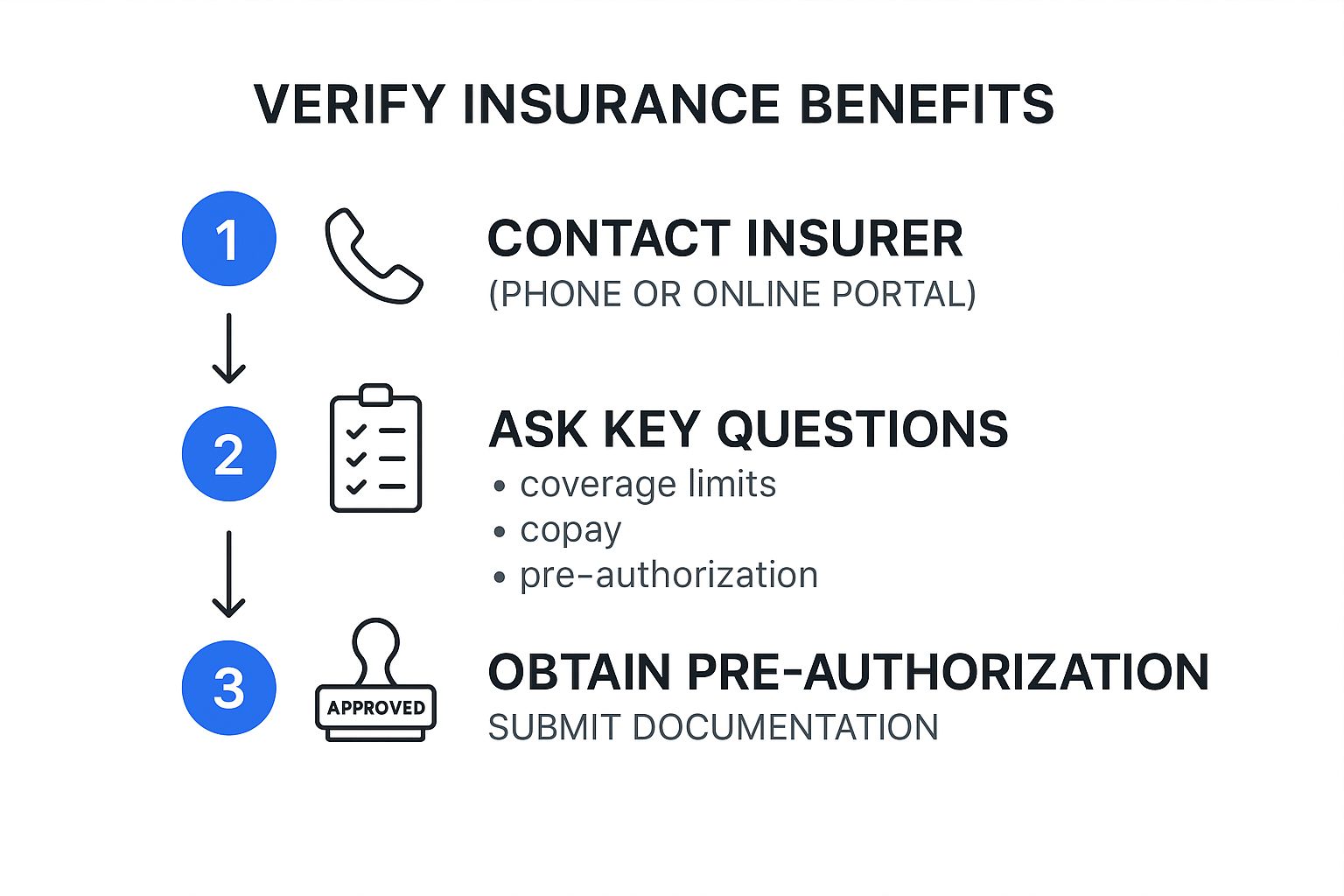

How to Verify Your Insurance Benefits Step by Step

Knowing your plan probably has some form of insurance coverage for rehab is one thing, but you absolutely can't assume you know the details. To head off any surprise bills and make sure the admissions process goes smoothly, you have to verify your specific benefits before you commit to a treatment program. This isn't just a good idea—it's the most important financial step you'll take.

Think of it this way: you'd never let a contractor start tearing down walls in your house without a detailed, written quote. Verifying your insurance is the exact same principle. It gives you a financial blueprint for your recovery, so you can focus on getting better, not on worrying about unexpected costs.

Start the Conversation with Your Insurer

The best place to start is by getting in touch with your insurance provider directly. You can usually do this one of two ways: call the member services number on the back of your insurance card or log into your online portal. While the portal is great for a quick look, a real conversation on the phone is almost always better for getting clear answers to tricky questions about rehab coverage.

This first call is where you pin down exactly what your policy covers. It can honestly be the difference between a fully covered stay and a shocking bill for thousands of dollars. Don't hesitate to be persistent and ask them to explain things until you're 100% clear on your benefits.

The global insurance market is getting bigger every year, with one recent report showing an 8.6% expansion. This growth reflects a greater focus on health services, which makes it even more vital for you to understand your policy. If you're interested in the bigger picture, you can read more about these global insurance trends from Allianz.

Ask the Right Questions

When you get an insurance representative on the phone, you'll want to have a list of questions ready. Being prepared ensures you get all the information you need in one go, without having to call back.

Here are the essential questions to ask:

- Does my policy cover residential, inpatient, and outpatient addiction treatment?

- What is my remaining deductible for the year, both for myself and my family?

- What will my copay and coinsurance be for these specific services?

- Is the treatment center I’m looking at considered in-network or out-of-network?

- What's my out-of-pocket maximum, and how much of it have I already met this year?

- Do I need to get pre-authorization before I can be admitted?

Getting straightforward answers to these will give you a complete and realistic picture of what you'll be expected to pay.

Securing Pre-Authorization for Treatment

That last question about pre-authorization (sometimes called prior approval) is arguably the most important one. This is the official green light from your insurance company, confirming they agree that treatment is medically necessary and that they will cover it under your plan.

Think of pre-authorization as a formal agreement. Skipping this step is one of the top reasons claims get denied, which could leave you on the hook for the entire bill.

Typically, the admissions team at the rehab facility will handle this for you. They'll submit the required clinical information—like your diagnosis, medical history, and proposed treatment plan—to your insurer to make the case for why you need care.

This infographic breaks down the process of verifying your benefits and getting that all-important pre-authorization.

It lays out a simple, three-part path that takes you from feeling uncertain to having confirmed coverage. This way, there are no financial roadblocks on your journey to recovery.

Making the Call: In-Network vs. Out-of-Network Rehab

Choosing between an in-network and an out-of-network rehab facility is one of the biggest financial decisions you'll face on the path to recovery. It’s a choice that can literally save you thousands—or even tens of thousands—of dollars. Getting a handle on the difference between these two paths is the first step to protecting your wallet.

Think of in-network providers as trusted partners of your insurance company. They’ve already shaken hands on a contract, agreeing to provide their services at a much lower, pre-negotiated rate. For you, this means a smoother ride—less paperwork, lower out-of-pocket costs, and no surprise bills.

Going out-of-network, on the other hand, is like hiring a specialist who doesn't work with your insurance. They haven't agreed to any special rates, so they can charge whatever they want. Your insurer will likely cover only a small fraction of that bill, if they cover it at all, leaving you on the hook for a massive balance.

The Real-World Cost Difference

The financial gap between in-network and out-of-network care isn't just a few bucks; it can be staggering. Let's walk through a quick example to see how this actually plays out.

Imagine a 30-day inpatient program with a sticker price of $30,000. Here’s how your insurance might break it down:

- In-Network Scenario: Because of their contract, your insurer's pre-negotiated rate is just $18,000. After you meet your deductible, your plan might cover 80% of that amount. You’d owe the remaining 20%, which comes out to $3,600 (plus your deductible).

- Out-of-Network Scenario: The facility charges the full $30,000. Your insurance company might only agree to cover 50% of what they decide is a "reasonable" cost—let's say they decide that's $15,000. That leaves you responsible for the other $15,000, on top of your deductible.

This simple math shows why staying in-network is almost always the smartest financial move. As the need for addiction treatment grows—the global rehabilitation medical services market is projected to hit $23.34 billion with an 8.7% annual growth rate—strong insurance coverage for rehab is more critical than ever to make care affordable. You can see the full scope of this growth by exploring these rehabilitation market insights on archivemarketresearch.com.

How to Find In-Network Rehab Centers

The good news is that finding a list of approved, in-network facilities is pretty simple. Your insurer wants you to use these providers, so they make it easy to find them.

- Check Your Insurer’s Online Portal: Just log in to your insurance company's website. You should find a "Find a Doctor" or "Provider Directory" tool where you can search for in-network substance use treatment centers near you.

- Call Member Services: Flip over your insurance card and dial the number on the back. A representative can quickly look up and even email you a list of local, in-network rehabs.

- Ask the Rehab Facility Directly: When you're calling around to potential treatment centers, make this one of your first questions: "Are you in-network with my insurance plan?" The admissions team will be able to tell you right away.

When you choose an in-network provider, you are not just saving money; you are choosing a facility that has been vetted by your insurance company, which often adds an extra layer of quality assurance.

When Out-of-Network Is the Only Option

Sometimes, you might not have a choice. In rare cases, an out-of-network facility might be the only one that offers a highly specialized program you need, like for a specific dual diagnosis. It could also happen if there are simply no in-network options in your area.

If you find yourself in this tough spot, don't panic. You'll need to immediately contact your insurer and request a network gap exception. This is basically an appeal for them to cover the out-of-network facility at the in-network rate because a suitable alternative just doesn't exist. It takes some persistence and paperwork, but it can be a financial lifesaver. Before committing to a level of care, be sure to check out our guide on the differences between inpatient and outpatient rehab to make sure it’s the right fit for you.

Getting a Handle on Out-of-Pocket Costs and Finding Help

Even with a great health plan, insurance rarely covers 100% of the bill for rehab. Knowing what you'll be responsible for financially is crucial, so costs don't become a roadblock to getting the help you need. You'll almost certainly have some out-of-pocket expenses, but if you know what to expect, you can manage them.

Think of your insurance policy as a cost-sharing partnership. Your insurer picks up the lion's share of the bill, but you're on the hook for your part—the deductible, copayments, and coinsurance. The good news is that this isn't endless. Once you hit your out-of-pocket maximum for the year, your insurance plan steps in to cover 100% of all approved services from that point on.

What Your Policy Might Not Cover

While the core components of your treatment are usually covered, some services might not be. It’s important to get a clear picture of these common exclusions to avoid any nasty surprises on your final bill.

Be on the lookout for specific limits or exclusions for things like:

- Length of Stay: Your plan might cap the number of covered days for inpatient care, often at 30 or 60 days per year. If you need to stay longer, you’ll have to cover the cost of that extra time yourself.

- Holistic or Experimental Therapies: Services like acupuncture, massage therapy, or equine-assisted therapy are often seen as "complementary" rather than medically essential, so they frequently aren't covered.

- Private Rooms and Luxury Amenities: Insurance is designed to pay for effective medical treatment, not five-star accommodations. If you opt for a facility with high-end perks, expect to pay for them out of your own pocket.

The golden rule? Always, always call your insurance company and confirm coverage for specific therapies before starting treatment. It's the best way to prevent misunderstandings down the road.

Real-World Strategies to Make Treatment Affordable

Seeing a big price tag can feel overwhelming, but don't let it discourage you. You have more power than you think to make treatment affordable. That first number you see is rarely the final word.

The need for this kind of care is staggering. According to the World Health Organization, about one-third of the global population has a condition that would benefit from rehabilitation. That figure has skyrocketed by 63% since 1990, showing just how critical this issue has become. You can dig deeper into the global need for rehabilitation from the WHO.

If you're worried about the cost, here are a few practical steps you can take:

- Ask for a Payment Plan: Most rehab centers are more than willing to work with you. They can often set up an interest-free payment plan, letting you spread the cost out over several months or years to make it manageable.

- Look for Scholarships or Grants: A surprising number of non-profits offer financial aid specifically for addiction treatment. The Substance Abuse and Mental Health Services Administration (SAMHSA) is a fantastic place to start your search for grants.

- Check Out State-Funded Programs: Every state gets government funding to offer affordable rehab to residents who can't otherwise afford it. Get in touch with your state's mental health or substance use agency to find out if you're eligible.

- Try Crowdfunding: Platforms like GoFundMe can be an incredible way to rally your community—friends, family, and even strangers—to help you cover the cost of treatment.

Remember, your right to treatment is protected by law. If your insurer denies a claim that you and your doctor believe is necessary, you have the right to appeal. A denial is just the start of a conversation, not the end of the road.

The admissions team at your rehab facility can be your biggest advocate here. They deal with insurance companies all day long and know exactly how to navigate the appeals process. They can help you pull together the right paperwork to fight a denial and get the coverage you're entitled to.

Your Checklist for Maximizing Rehab Coverage

Trying to figure out your insurance benefits can feel overwhelming, especially when all your energy should be on getting well. But if you know what to look for, you can navigate the process with confidence and get the most out of your insurance coverage for rehab.

Think of this as your personal action plan. It's a straightforward guide to cut through the confusion and make sure financial surprises don't get in the way of the care you need. Let’s break down the most important steps.

Your Four-Point Action Plan

This isn't about learning complex insurance jargon. It’s about taking a few powerful, practical steps that can save you a lot of money and stress during the admissions process.

-

Always Verify Your Benefits First: Never just guess what your policy covers. The first thing you should do is call the member services number on the back of your insurance card. Ask for specific details about your deductible, copays, out-of-pocket maximum, and what they cover for different levels of care, like inpatient, outpatient, and detox.

-

Prioritize In-Network Facilities: The cost difference between a facility that’s in-network versus one that's out-of-network can be massive. You'll almost always save a significant amount of money by sticking with providers your insurance company has a contract with. Start by asking your insurer for a list of approved, in-network rehabilitation centers. Our guide to rehabilitation centers can also help you understand how to find and choose the right facility for your needs.

-

Confirm Pre-Authorization is Complete: Pre-authorization is basically getting the green light from your insurance company, confirming that they agree your treatment is medically necessary. While the rehab center's admissions team will typically handle this for you, it's ultimately your responsibility to double-check that it’s been approved before you officially start treatment.

Skipping pre-authorization is one of the most common—and most expensive—mistakes people make. Moving forward without it is a huge gamble that can lead to a denied claim, potentially leaving you on the hook for the entire bill.

- Be Your Own Best Advocate: Keep a log of every conversation you have with your insurance company. Note the date, time, and the name of the person you spoke with. Don't hesitate to ask questions until you feel you completely understand. And if a claim gets denied, remember you have the right to appeal that decision.

Following these four simple steps puts you in the driver's seat. It empowers you to make smarter choices, avoid unexpected costs, and keep your focus where it belongs: on your recovery.

Frequently Asked Questions (FAQ)

Will my insurance premiums go up if I use it for rehab?

No. Thanks to the Affordable Care Act (ACA), insurance companies are prohibited from raising your rates or dropping your coverage for having a pre-existing condition, which includes a substance use disorder. Using your benefits for treatment will not result in higher premiums.

What if my insurance company denies my claim for rehab?

A denial is not the final word. First, carefully read the denial letter to understand the reason. You have the right to file an internal appeal with your insurance company. If that is unsuccessful, you can request an external review by an independent third party. The admissions team at your chosen rehab facility can provide significant help with navigating the appeals process.

Will my employer find out I'm in rehab?

No. Your privacy is protected by the Health Insurance Portability and Accountability Act (HIPAA). Even if you have an employer-sponsored plan, your employer cannot access your personal health information. Your insurance provider is legally required to keep all details of your treatment confidential.

Does insurance pay for luxury or executive rehab?

Typically, no. Insurance covers services that are deemed "medically necessary," such as detoxification, therapy, and medical supervision. It does not cover luxury amenities like private suites, gourmet meals, or resort-style facilities. While a luxury center may be in-network, your plan will only cover the standard treatment costs, leaving you responsible for the additional charges for premium amenities.

Sorting through your insurance is a critical first step on the path to recovery. At StartDrugRehab.com, we're here to give you the resources and support you need to find the right care with confidence.